ZAFAR & ASSOCIATES - LLP | Customs Law Services - Pakistan

Customs law is a duty, tax, charges, or imposts levied by the government on imported or exported goods, in contradistinction to internal taxes, such as excise duties or sales taxes, customs duty is applied to the movement of goods irrespective of sales or purchase, it is a tax which is applied indirectly by government, applicable only on goods and not on services.

Customs law is a duty or tax which is levied by the Federal Government on import of goods into and export of goods from Pakistan. Quantum of customs duty depends upon the provisions of Customs Act, 1969, Cusoms Rules 2001 and Customs Tariff 2021 along with Notifications, Circulars, Case Laws and Annual Finance Acts.

The objective of this law is to provide for the proper enforcement of customs procedures regarding the determination, payment, collection and refund of customs duty, as well as the exportation and importation of goods. To protect the imports and exports of goods for achieving the policy objectives of the Government. To co-ordinating legal provisions with other laws dealing with the foreign exchange such as the Foreign Exchange Regulation Act, 1947.

Interpretation of Customs Act in Pakistan

The Customs Act, 1969 is a special statute by nature, termed as fiscal as well as penal. The well known canons of interpretation of such statute are:

Where a statute creates special offence and lays down a special procedure for the trial of such offences it is that procedure which must be followed and not the ordinary and general procedures.

Where a special offence is created by a statute and the mode of punishment is provided, it is that mode which is to be followed and no other mode.

Where in a statute there are both general provisions as well as special provisions for meeting a particular situation, then it is the special provisions which must be applied to that particular case or situation instaed of general provisions.

Fiscal statute are to be construed strictly so far as liability to tax is concerned, but not in regard to proceeding in realisation of tax.

No word in statute is to be lightly inferred as surplusage or as redundant.

Notification generally to be construed as prospective unless otherwise expressly stated.

The subject should not be made liable for tax unless such a step is warranted by the clear provision of the statutes.

Where there is doubt in the matter an interpretation favourable to the subject should be preferred.

There is no equity, intendment and presumptions as to tax. Nothing is to be read in, nothing is to be implied. One can only look into fairly at the language used.

Interpratation helping evasion of tax is not permitted.

Substance and not form is to be taken into consideration.

Benefit should always be given to the subject in case of doubt.

A fiscal provision can be made with retrospective effect by the legislature by clear words whereas a penal provision cannot be enacted with retrospective effect. The procedural change is always considered with retrospective effect.

The provisions of the Customs Act have to strictly construed as their infriction involves penal consequences and therefore, the burden of bringing unlawful import was on the Customs Authorities. In case they failed to discharge the burden the benefit of doubt must go to the accused person.

While construing the fiscal statute one must read words and interpret them clearly.

If the order passed is illegal then perpetual rights cannot be gained on the basis of an illegal order and in such a case even the principle of locus poenitentiae would not apply.

If there is passed departmnetal practice which is being carried on the wrong interpretation and in violation of law, then such practice has to be stopped and interpration in accordance with law has to be given effect.

Beneficial legislation being remedial and curative would be given retrospective effect. Beneficial fiscal legislation can, if need be, be regrded as applying retrospectively. Beneficial provisions of law are always retrospective in nature untill and unless they have been made prospective by their implication. Remedial and curative statutes are always retrospective in nature.

When special statute provides something to be done in a particular manner the general provisions are ousted. Whereever the term 'include' is used the intention of legislature was to give it a widest possible meaning.

The court always lean in favour of constitunality of legislation unless it is ex-facie violative of constitutional provision.

Provisions of statute would have to be construed harmoniously so as to advance the purpose of substantive provision of law and to avoid conflict. No provision can be placed into service in order to defeat the real object of the main provision. Effect must be given, if possible, to all the words used in statutory provision.

Foreign Exchange Regulation

Foreign businesses that import goods or provide services in Pakistan must comply with the Foreign Exchange Regulation Act, 1947 and rules issued by the SBP, The Customs Act, 1969 and Sector-specific laws (for example, the Banking Companies Ordinance and rules and regulations of the SBP relating to the banking sector).

Pakistan Customs is tasked with ensuring that following tasks are performed in the legal prescribed manner:

Import & Export of legitimate cargo

Trade Facilitation

Trade Regulator

Preventive (Control of contraband Goods)

Revenue Collection

Register for Customs

In order to access the online Customs portal WeBOC, the person would first have to register themselves with Federal Board of Revenue.

Application Form for Registration or Issuance of WeBOC User ID can be accessed by clicking here

Revalidation of WeBOC

Periodical personal appearance of the User ID Holder before Deputy / Assistant Collector User-ID Re-Validation section with original CNIC and supportive documents.

Process of taking digital picture and thumb impression of the applicant upon personal appearance.

Visit of the Business premises (wherever required).

Procedure for Registration

Submission of application to Deputy / Assistant Collector WeBOC User-ID Section, along with supportive / required documents.

Personal appearance of applicant before Deputy / Assistant Collector User-ID Section with original CNIC.

Process of taking digital picture and thumb impression of the applicant upon personal appearance.

Visit of the Business premises (wherever required).

Acceptance / Rejection of Application.

Creation of User-ID in case of acceptance of application.

Issuance of Login-ID and automatic sending of computer generated password to the applicant through email.

Types of Registration

Following types of registration/WeBOC user IDs are given on the basis of eligibility criteria:

Trader

Commercial (i.e. Manufacturer, Manufacturer-cum-Exporter, Commercial Importer, Commercial Exporter)

Non-Commercial

Ship-Breakers

Trust / Non-profitable Organization

Diplomatic Cargo (Embassies)

Government Department

Courier Services

Customs Agent

Bank Users

Bonded Carriers

Shipping Lines

Warehouse

Evaluating Pakistan Customs Tariff

Goods imported and exported from Pakistan are liable to rates of Customs duties as prescribed in Pakistan Customs Tariff. Customs duties in the form of import duties and export duties constitute about 37% of the total tax receipts. The rate structure of customs duty is determined by a large number of socio-economic factors. However, the general scheme envisages higher rates on luxury items as well as on less essential goods. The import tariff has been given an industrial bias by keeping the duties on industrial plants and machinery and raw material lower than those on consumer goods.

National Entry & Exit Points

Customs Duty Drawback

FBR has devised a Centralized System of online payment of Customs Duty Drawback payments directly in the bank account of the Exporters. For this purpose members are requested to update their WeBOC profile. In the given Bank account details area in the system IBAN detail row is added wherein members are required to add their complete Bank’s IBAN number of same Bank Account whose details are already available in WEBOC profile to receive Custom Duty Drawback. Members are advised to do needful ASAP to avail electronic transfer facility for Customs Duty Drawback payments.

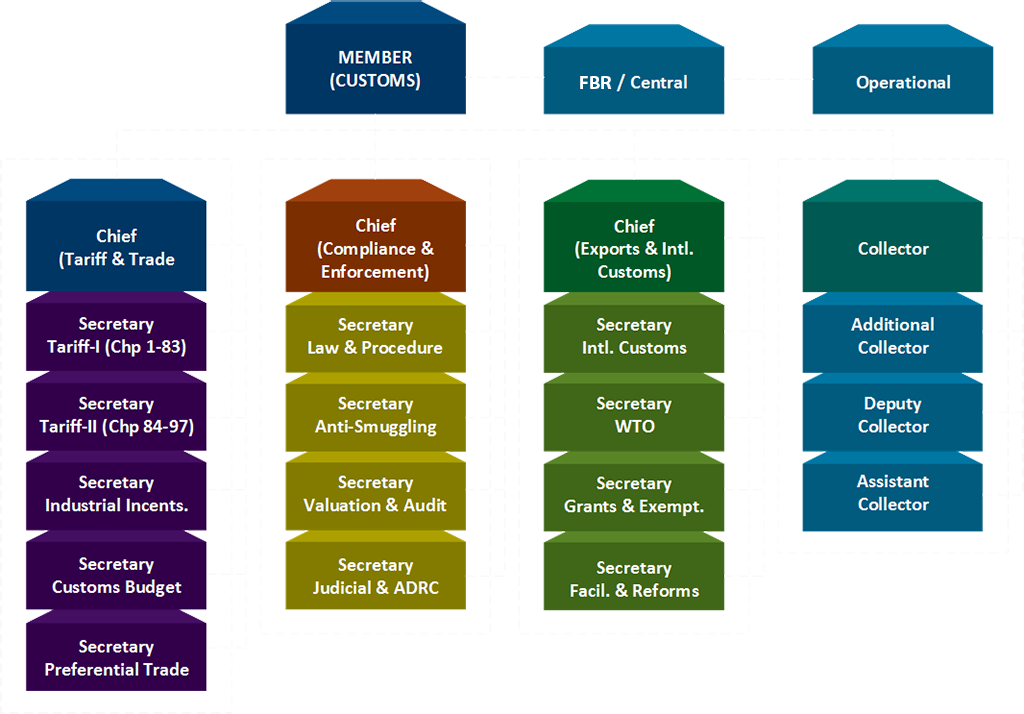

Central & Operational Hierarchy

World Customs Organisation (WCO)

The World Customs Organization (WCO), established in 1952 as the Customs Co-operation Council (CCC) is an independent intergovernmental body whose mission is to enhance the effectiveness and efficiency of Customs administrations.

Today, the WCO represents 182 Customs administrations across the globe that collectively process approximately 98% of world trade. As the global centre of Customs expertise, the WCO is the only international organization with competence in Customs matters and can rightly call itself the voice of the international Customs community.

As a forum for dialogue and exchange of experiences between national Customs delegates, the WCO offers its Members a range of Conventions and other international instruments, as well as technical assistance and training services provided either directly by the Secretariat, or with its participation. The Secretariat also actively supports its Members in their endeavours to modernize and build capacity within their national Customs administrations.

Our Core Competencies

Collaborative Skillset

Collaborative lawyers trust the wisdom of the group; lone wolves and isolationists do not do any good anymore.

Emotional Intelligence

Distant, detached lawyers are relics of the 20th century, the market no longer wants a lawyer who is only half a person.

Technological Affinity

If you can not effectively and efficiently use e-communications, and mobile tech, you might as well just stay home.

Time Management

Virtually a substantial part of lawyers difficulties in this regard lie with their inability to prioritise their time.